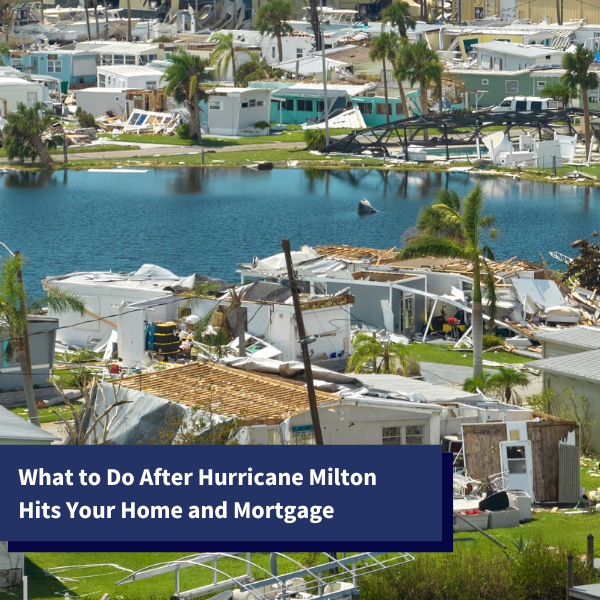

Hurricane Milton is expected to be the ‘storm of the century,’ and over 5.5 million people were urged to vacate Florida’s western coast. Many of these people may return to a severely damaged home, or complete loss of property. Those who chose to stay may witness the damage firsthand themselves. In either case, homeowners are going to have many questions regarding their homes, and their mortgage, in the aftermath. If your home has suffered damage to any extent after Hurricane Milton, it is important to take the steps below.

What to Do After Damage from Milton?

Hurricane Milton, and its aftermath, is an emergency and you will need immediate help. The first steps to take are as follows:

- Contact the Federal Emergency Management Agency (FEMA) by calling 800-621-3362, in person at a disaster recovery center, or by registering with them online.

- Call your homeowner’s insurance company. If you have additional coverage, such as that covering flood damage, make sure you have the policy number when you call or that you contact the separate company, if applicable.

- Call your mortgage servicer. This is not the company that owns your mortgage. This is the company that handles your payments and that you pay directly. Your mortgage servicer may have certain options available that can help cover your mortgage payments, if necessary.

What to Do if You Cannot Pay Your Mortgage?

Hurricanes, and other disasters like them, cause devastating damage. You may have to find a new place to live, temporary or otherwise, purchase new food and personal items, and face a number of other expenses. It is understandable if, during this time, you cannot pay your mortgage. If Milton has impacted your ability to pay, you may be able to ask your servicer for a mortgage forbearance.

With a forbearance, you may be able to stop making mortgage payments for six months to one year. While you will not have to make monthly payments, you will still accrue interest on those payments. Still, your lender cannot charge late fees or report your missed payments to the credit bureaus. Your lender will likely ask that you catch up on any missed payments once the forbearance period is over. You can typically do this by slowly repaying it every month for a period of time, on top of your regular mortgage payments, or you and your lender may agree to a loan modification.

What Federal Aid is Available?

Direct federal aid consists largely of loans provided by the Small Business Administration (SBA). Despite the name of the agency, the SBA oversees the delivery of disaster-related loans to families and individuals. The SBA provides loans up to $200,000 to cover construction or renovation costs for primary residences. If you are a homeowner, the SBA will also provide loans up to $40,000 to replace or repair personal items such as furniture, clothing, vehicles, and appliances.

You may be able to obtain a grant from FEMA if there are gaps between your insurance coverage and SBA loan. You can also use this type of grant for basic home repairs insurance will not cover, temporary accommodations, and medical and child care caused by the hurricane.

The Federal Housing Administration (FHA) also has a program that can help you rebuild your current home or purchase a new one. The FHA insures mortgages for homeowners when their property is damaged or destroyed during a disaster. You are not required to make a down payment.

Do I Have to Pay My Mortgage if My Home Was Completely Destroyed?

It is a sad but true fact that Hurricane Milton will likely completely destroy the homes of many people. Unfortunately, the destruction of your home does not allow you to continue paying your mortgage. You must continue making mortgage payments, if you are able to, until you can speak with your mortgage lender or servicer. If you cannot afford to, make sure you contact your lender or servicer as soon as possible.

You should also understand the relief options available to you after being impacted by Milton. In addition to avoiding penalties associated with not paying your mortgage, continuing regular payments is important for another reason. If you apply for a loan from the SBA, the agency will run a credit check before conducting an inspection of your property. It is important to continue paying your mortgage so missed payments do not lower your score at the time you need an SBA loan.

What if You Cannot Contact Your Mortgage Servicer?

After a disaster such as Hurricane Milton, it is not always easy to contact the people and companies you need to speak to most. There is a chance that you will not be able to contact your mortgage servicer right away. If your loan is guaranteed by the Department of Veterans Affairs, Freddie Mac or Fannie Mae, or if it is insured by the FHA, the mortgage servicer is expected to contact you.

If your servicer cannot reach you, they can grant a 90-day forbearance period. They can grant this forbearance verbally, even if they cannot contact you immediately. Still, after Milton and any other disaster, always answer any phone call you can and open any mail you may receive.

What if You are Already in Foreclosure?

Facing disclosure is devastating to too many households across Florida. While you are trying to fight a foreclosure initiated by your lender, the last thing you want to think about is losing the home you have been fighting so hard for to be severely damaged by the hurricane. Federal agencies guide and advise mortgage servicers and lenders and their recommendations will vary depending on the disaster and your personal situation.

Our Foreclosure Defense Attorneys in Fort Lauderdale Can Help with Your Case

Hurricane Milton is going to devastate many households in Florida. If you are facing foreclosure in Florida, want to learn more about your options to save or repair your home, or need guidance on other alternatives, our Fort Lauderdale foreclosure defense attorneys can help. At Loan Lawyers, we will answer all of your questions and help you understand the best way to move forward. Call us today at (954) 523-4357 or contact us online to schedule a free consultation.

- About the Author

- Latest Posts

Matis Abarbanel is the founding partner and senior attorney at Loan Lawyers in South Florida. He focuses his practice on consumer rights, helping homeowners navigate issues such as foreclosure and financial hardship. Matis also brings a wealth of experience from his previous work in personal injury law. As a devout Chasidic Jew, he is committed to making a positive impact in his community and dedicates his efforts to charitable initiatives through his non-profit organization, The Center, which aids at-risk Jewish youth. Matis actively serves clients across South Florida and is passionate about empowering individuals to secure their rights and achieve a better future.